Jon Salon: BCI tripled private equity outlays in 2025 to tap into ‘complex’ market

Insights

![]()

By Kirk Falconer

Published: June 2026

In his first interview since becoming BCI’s global head of private equity, Jon Salon tells Buyouts about the factors driving robust PE investing and distributions in 2025 and his plans for the strategy going forward.

BCI’s private equity group ramped up investing last year to take advantage of fresh opportunities presented by a knotty market environment.

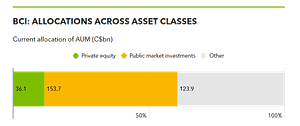

The C$314 billion ($221 billion) Canadian pension system put C$6.7 billion of capital to work in PE fund and direct investing in 2025, more than triple the C$2.2 billion of a year earlier, according to BCI’s 2026 annual report, issued last week. Of the total deployed, fund commitments accounted for C$3.6 billion, while directs and co-investments represented C$3.1 billion.

The jump in BCI’s direct activity was especially large, amounting to nearly four times the C$800 million invested in 2024. As a result, the share of NAV captured by directs and co-investments last year increased to 49 percent, up from the prior year’s 44 percent.

BCI’s vigorous investing in 2025 owed to a PE market that is “complex and a bit dislocated,” Jon Salon, global head of private equity, told Buyouts in his first interview since assuming his current role. Market conditions, he said, allowed for “opportunistic investing” by the pension, which unlike many of its LP peers has no significant liquidity issues.

“Across the deal pipeline, we found some good fits,” Salon said. Opportunities encountered included high-quality technology companies impacted by trends like AI and “trading at a discount,” he said.

Among the 23 direct deals closed last year were BCI’s co-control acquisition, alongside Ethos Capital and White Mountains Insurance Group, of BroadStreet Partners, and its acquisition with AEA Investors of Pave America.

Directs were pursued with a more selective group of GPs, following a 30 percent cut in the number of fund partners. “There were too many relationships to manage effectively, and we needed a sharper focus on our partners and portfolio,” Salon said. The freed-up capital, he noted, was mostly channeled into bigger re-ups with core relationships.

In addition to PE firms identified above, BCI’s existing roster of fund partners includes top brands like Advent International, Bain Capital, CVC Capital Partners, Hg and Leonard Green & Partners.

Perhaps surprisingly, BCI saw even more capital returned in 2025 than it put out, with distributions reaching C$7 billion. Distributions by GPs were part of the mix, though “lighter than you’d want them to be,” Salon said. For this reason, the pension also targeted sales of direct interests, such as its stake in Hayfin Capital, together with secondary sales.

BCI executed C$1.9 billion of fund stake stake sales, last year. Secondaries, Salon said, are useful to BCI “as a way to generate liquidity and to re-invest.”

Graphic by Mariam Lobjanidze

Source: Buyouts LP Database, data last updated on June 26, 2026.

Capital solutions debut

BCI’s robust PE outlays in 2025 were driven by a strategy emphasizing global buyout and other opportunities in consumer, financial and business services, healthcare, industrials, and technology, media and telecom sectors. A key contributor was the pension’s capital solutions program, officially launched in May.

The program was designed to provide flexible capital to structured equity, GP solutions and strategic opportunities, with a focus on preferred equity, continuation vehicles, recaps and minority stakes. As such, it addresses “the complexity in the market and the challenge of creating liquidity,” Salon said.

As traditional buyouts offered fewer opportunities last year, he said, flexible investing filled the void with “a full pipeline of CVs, structural equity and other non-traditional deals.”

BCI closed C$1 billion of related transactions in 2025, comprising four CV investments and two structured equity investments. They included the CV for Ethos-backed Identity Digital, in which TPG GP Solutions, Neuberger, AccelKKR, Coller Capital and CVC Secondary Partners also participated.

Capital solutions gives BCI a direct investor role in GP-led secondaries that is unique among LPs, even the very largest. As opportunities are sourced from both fund partners and a wide network of other GPs and institutional relationships, it promises to “generate good returns,” Salon said.

Another contributor to deployment last year was the venture and growth program, which concurrently hit an AUM milestone of C$1 billion. It was responsible for “good fund commitments and good co-investments,” Salon said, with the latter illustrated in the Planet First Partners-led financing of Photonic.

Venture and growth lends more exposure to high-growth technology sectors of interest to BCI, Salon said, reflected in 2025 positions built across AI infrastructure, cybersecurity and quantum computing. Further, it has allowed the pension to “progressively invest in bluechip funds,” he said.

One measure of just how far BCI has progressed as an investor alongside Silicon Valley’s Who’s Who is its spot in this year’s financing of AI giant Anthropic, led by Altimeter Capital, Dragoneer, Greenoaks and Sequoia Capital.

Graphic by Mariam Lobjanidze

Source: BCI Corporate Annual Report 2025-2026

More onus on directs

On balance, BCI’s PE portfolio assets rose slightly last year to a total of C$36.1 billion from C$33.6 billion in 2024. Private equity’s share of all pension assets stood at 13.6 percent, compared with a target of around 15 percent.

One area in which PE strategy results were somewhat muted was performance. The portfolio earned an 8.1 percent annualized one-year return in 2025, below its 11.9 percent benchmark, according to the annual report. On the other hand, longer-term performance topped benchmarks, evidenced in the 12.1 percent five-year return and the 14.5 percent 10-year return.

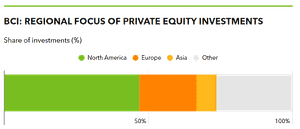

Salon attributes the dip in returns to broader PE industry underperformance, “especially on the funds side.” Directs and co-investments instead “beat the benchmarks,” he noted, in keeping with their role as the portfolio’s alpha generator. Because of this, the near-term plan is to increase directing investing, bringing these directs-to-funds investment ratio to roughly 55:45.

BCI’s PE group experienced outsized growth during the 10-year tenure of Salon’s predecessor, Jim Pittman, with AUM expanding more than five times. Salon said he intends to stay on the growth path by “selectively adding new programs and sharpening the execution.”

Agenda items include working with fund partners to ensure greater benefits “from the fees we pay them” and “more deliberate active management” on the directs side, he said. Salon will also assess “exposures in the portfolio” as a way to “mitigate against risk and volatility.”

Based in BCI’s New York office, Salon joined the pension in 2024 from Evernorth’s MDLIVE, where he was president and CEO. Before, he was a founding partner of Bedford Funding, a specialist in buyout and growth equity investing in healthcare and technology companies.

Republished with permission. Read the original article on Buyouts Insider – subscription may be required.